Measures were introduced, that increased the normal notice period due to the Covid Pandemic. That meant from the 29th of August 2020 that the typical (Section 21) notice period was increased from 2 months to 6 months. This was introduced with the intention of protecting Tenants affected by the Pandemic and being unable to afford to pay their rent. This also gave blanket protection in some instances to Tenants and it is also argued that the introduction of the 6 month notices led to some Tenants taking advantage of this protection by not keeping up with their rental obligations.

The extended notice period, was a temporary measure that was introduced and the road map to come back to the original notice period length (2 months for a section 21 is coming into place soon). There has also been a ban on bailiff-enforced evictions, which will be lifted on the 31st of May 2021. This has meant that Landlords who have served the correct notices, and the Tenants haven’t vacated on the expiry of the notice (even if they have obtained a court order) haven’t been able to get possession. However, Blackpool and Fylde Coast Landlords will now be able to apply to the Courts for Bailiffs for Evictions where required.

Notice period will be reduced to 4 months from the 1st of June 2021 (exemptions for some more serious cases, as detailed below). We will await confirmation when the next step is taken to reduce the Section 21 notice period back to 2 month’s, however it is clear that this will not take place until at-least October 2021. A revised Section 21 Notice will be required for the 4 month notices.

It is also worth taking into consideration that the Government has pledged (Queens Speech, December 2019) the abolishment of the Section 21, maybe the Government will take this opportunity to make the change.

If you are looking to gain possession and you face a problematic Tenant and the Tenant doesn’t vacate on the expiry of the Tenancy we face an issue of huge backlogs at the Courts or Bailiffs. Solicitors seem to be overwhelmed currently, which also will lead to delays.

My recommendation is to have Rent and Legal Protection (or similar Insured Rent Guarantee Product in place), to avoid extremely costly and stressful issues in the future. Especially with the uncertain Economic times we face.

Exemptions to the 4 month notices are:

anti-social behaviour (immediate to 4 weeks’ notice)

domestic abuse in the social sector (2 to 4 weeks’ notice)

false statement (2 to 4 weeks’ notice)

over 4 months’ accumulated rent arrears (4 weeks’ notice)

breach of immigration rules ‘Right to Rent’ (2 weeks’ notice)

Your Tenant has vacated, you are looking to get it let quickly and to the right tenant, have you considered the steps and the action needed so you can secure the right tenant for the Long Term, a Tenant that will look after your property, the best market rent and the least hassle possible?

I have let my own properties over 60 times over the last 9 years and at Martin and Co Blackpool, St Annes and Lancaster we do approximately 250 Lets per year. This has given me a great idea into what needs to be done to get your property in the best positions for marketing. Here’s my guide to getting your property ‘Show Home Ready’. Follow these steps and your Buy to Let Investment will Make you More Money, Let Quicker and Give you Less Hassle.

Clean – yes I am reminding you to clean the rental property, as I have seen soo many examples over the years as a Letting Agent, where the property is just in an acceptable condition. I would especially emphasise hobs, oven, mould in bathroom areas, windows, carpets etc. I would diarise to have the property to this standard each time a Tenant vacates your property, regardless of how ‘good’ you believe the tenant may have left the property in. Is there any Clutter in the property? If so that needs to be fixed, clutter will affect the pictures of your property and not put the property in the best light when marketing the property?

Repairs -I have developed a model of when I conduct a checkout to determine the work I carry out, I call it the E.S.N. model, details of which I will discuss in a latter post. To summarise make a list of everything that needs doing now and what would be good to do. Getting the essential repairs done prior to marketing and review the items what would be good to do and see if it makes financial sense to do so or plan them in your future plans. Makesure all appliances, boilers etc work. If prepayment metered is their electricity and gas at the property? Lightbulbs all working?

External Areas – yes this part of the property is still part of your property! Curb appal is everything. Modern fascias and well maintained doors are key. I love a nice door to a property. Have you considered a nice house number plaque? A decent door bell? Garden areas need to be cleaned, tidied up and always jet wash any entrances, patio areas. Makesure bins are in a dedicated area and that they aren’t full of rubbish (vacating tenants will fill waste bins in the process of them vacating).

Keys – ensure your outgoing Tenant has returned all sets. Ensure you have spare keys, I recommend you to have three sets all times for your properties.

Compliance – before you Let your poperty you will require an Energy Performance Certificate, Electrical Safety Certificate and a Gas Safety Certificate (if you have a gas), these are as a minimum for HMO’s, Block of flats etc more compliance documents will be requited. Get all of these in place before marketing your property, as you may need to get works done if they dont meet requirements, which may also cause some mess etc in the Property.

Landlord Insurance – ensure you have relevant Landlord insurance for your property. if it is coming to end soon, shop around to see what you can do to save money on your current policy

Freshen Up – I know some Landlords would disagree and argue it doesn’t make financial sense, but I would always look at decorating after a tenant moves out. I also look at flooring and I emphasise Kitchen and Bathrooms and will always try and makesure these areas look ‘fresh’.

After you have carried out these Steps you will be able to enjoy securing higher rents, renting out your property quicker and increasing your chances of securing a long term tenant and a ‘better’ Tenant. My Clients that follow these steps have managed to secure rent increases and let their properties significantly quicker, my office currently Lets all of our Properties within 8 days on Average, main reason is because of the way we prepare our properties for Marketing.

If you would like to discuss your Property Portfolio, please contact myself below.

Summary of Energy Performance Certificates and What You as a Blackpool Landlord Need to Do.

What is an Energy Performance Certificate?

An Energy Performance Certificate (EPC) is to the inform the person who will use the building how costly the building will be to Heat and Light and what the likely Carbon Monoxide Emissions. The idea is for the EPC to promote more efficient buildings For Sale or For Rent and by measuring performance drive Efficiency Ratings of Properties. The property will be rated A – G, it is possible for the property not to score a banding due to poor efficiency. The report also provides recommendations on how to make your property more efficient.

A certificate is Valid for 10 years, compared to a Gas Safety Certificate for example which would only be valid for 1 year. You can get this arranged by a qualified EPC surveyor, your local Agent should be able to put you in touch with a reputable source.

If you don’t have your EPC to hand and don’t know if it is Valid, you can contact your Letting Agent to confirm or alternatively go on to the http://www.epcregister.com, enter the address of your rental property and you will be able to find the EPC certificate for your property. The certificate will detail current rating, when EPC expires and any recommendations to improve the efficiency of the property.

I’m a Blackpool Landlord, how does Energy Performance Certificates affect me?

First of all it is compulsory for you to have an Energy Performance Certificate for any Property that is Let, the EPC must be E rated or above. A big misconception is that a valid EPC is only required when a tenant moves in to the property, that isn’t the case, a valid EPC is required throughout the lifetime of the tenancy (similar to a gas safety certificate for example). From 2025 it is important to point out all Properties need to have a rating of C or above, so if any properties fall short of that rating band when you are getting them assessed now, it is worthwhile looking at options to improve the rating of the property.

Is there any Funding available to make buy to let investment for energy efficient?

Yes, there is.

In the Blackpool and Fylde Coast Area a higher proportion of Housing Benefit tenants, which means if you are a Landlord with a tenant in receipt of qualifying benefits, you may be entitled to funding towards improving the energy efficiency of your property. One example is the Eco Funding Scheme, which currently has funding available for first time central heating systems. First time central heating systems can be fitted in properties even without a gas supply, a new combi boiler system will be fitted would be fitted under the scheme. To qualify for such schemes, the property needs to be tenanted and your tenant needs to be in receipt of benefits (child benefit is also a qualifying benefit). There will most likely be local companies who are pricing First Time Central Heating Systems in the area, we do work with two companies and would be happy to refer you to them. There is other energy efficiency measures provided under the scheme, the below article gives great insight into these options:

There is also currently have the Green Homes Grant, which you can use to improve the rating of your property (you are required to put a one third contribution to total cost, and funding is capped to a maximum of £5000).

How to get an Energy Performance Certificate?

You will find many EPC Assessors in your area, a simple google search will bring many that cover the area of your property. We use Sakander who covers the Lancashire area and his contact details are below:

When William the Conqueror invaded our fair shores in 1066, like all good kings, he needed to buy loyalty and raise cash to build his castles and armies. He did this by feudal law system and granted all the faithful nobles and aristocrats with land. In return, the nobles and aristocrats would give the King money and the promise of men for his army (this payment of money and men was called a ‘Fief’ in Latin, which when translated into English it becomes the word ‘Fee’… as in ‘to pay’).

These nobles and aristocrats would then rent the land to peasants in return for more money (making sure they made a profit of course) and the promise to enlist themselves and their peasants into the Kings Army (when requested during times of war). The more entrepreneurial peasants would then ‘sublet’ some of their land to poorer peasants to farm and so on and so forth.

The nobles and aristocrats owned the land, which could be passed on to their family (free from a fee i.e. freehold), while the peasants had the leasehold because, whilst they paid to use the land (i.e. they ‘leased it’ which is French for ‘paid for it’) they could never own it. Thus, Freehold and Leasehold were born (you will be pleased to know that in 1660 the Tenures Abolition Act removed the need of freeholders to provide Armies for the Crown!).

4.3 million properties in the UK are leasehold…

and 3,005 properties in Thornton-Cleveleys are leasehold. By definition, even when you have the leasehold, you don’t own the property (the freeholder does). Leasehold simply grants the leaseholder the right to live in a property for 99 to 999 years. Apart from a handful of properties in the USA and Australia, England and Wales are the only countries of the world adhering to this feudal system style tenure. In Europe you own your apartment/flat by using a different type of tenure called Commonhold.

The average price paid for leasehold properties in Thornton-Cleveleys is over the last year £137,177.

The two biggest issues with leasehold are firstly, as each year goes by and the length of lease dwindles, so does the value of the property (particularly when it gets below 80 years). The second is the payment of ‘ground rent’ – an annual payment to the freeholder.

Looking at the first point of the length of lease, the Government brought in the Leasehold Reform Act 1967, which allowed tenants of such leasehold property to extend their lease by upwards of 50 years. However, this was very expensive and as such only kicked the can down the road for half a century (when the owner would have to negotiate again to extend another 50 years – costing them more money, time and effort).

Ground rents on most older apartments are quite minimal and unobtrusive. The reason it has become an issue recently was the fact some (not all) new homes builders in the last decade started selling houses as leasehold with ground rents. The issue wasn’t the fact the property was sold as leasehold nor that it had a ground rent, it was that the ground rent increased at astronomical rates.

Many Thornton-Cleveleys homeowners of leasehold houses are presently subject to ground rents that double every 10 years.

That’s okay if the ground rent is £200 a year today, yet by 2121, that would be £204,800 a year in ground rent, meaning the value of their property would almost be worthless in 100 years’ time. One might say it allows for inflation, yet to give you an example to compare this against, if a Thornton-Cleveleys leasehold property in 1921 had a ground rent of £200 per annum, and it increased in line with inflation over the last 100 years, today that ground rent would be£9,864 a year.

This is important because the majority of leasehold properties sold in Thornton-Cleveleys during the last 12 months were apartments, selling for an average price of £87,222.

So, without reforms, the value of these Thornton-Cleveleys homes will slowly dwindle over the coming decades. That is why the Government reforms announced recently will tackle the problem in two parts.

Firstly, ground rents for new property will be effectively stop under new plans to overhaul British Property Law. Under the new regulations, it will be made easier (and cheaper) for leaseholders to buy the freehold of their property and take control by allowing them the right to extend the lease of their property to a maximum term of 990 years with no ground rent.

Secondly, in the summer the Government will create a working group to prepare the property market for the transition to a different type of tenure. Last summer the Law Commission urged Westminster to adopt and adapt a better system of leasehold ownership – Commonhold. Commonhold rules allow residents in a block of apartments to own their apartment, whilst jointly owning the land the block is sitting on plus the communal areas with other apartment owners.

These potential leasehold rule changes will make no difference to those buying and selling second-hand Thornton-Cleveleys leasehold property.

Yet, if you are buying a brand-new leasehold property, most builders are not selling them with ground rent (although do check with your solicitor). The only people that need to take any action on this now are people who are extending their lease. If you are thinking of extending the lease of your Thornton-Cleveleys property before you sell to protect its value, your purchaser may prefer to buy on the existing terms and extend under the new (and better) ones later (meaning you lose out).

Like all things – it’s all about talking to your agent and negotiating the best deal for all parties. Should you have any questions or concerns, feel free to pick up the phone, message me or email me and let’s chat things through.

Christmas Eve brought the news that Boris Johnson had conclusively agreed on a Brexit deal for the UK with the European Union. This gave optimism that the economic turmoil of leaving the EU would be radically reduced, yet what will this ‘trade deal’ do to the value of your Thornton-Cleveleys home and the mortgage payments you will have to make?

Since the summer, the Thornton-Cleveleys property market has been booming, yet many commentators have cautioned that the momentum cannot last. With unemployment and the end of the Stamp Duty Holiday on 31st March, the Halifax reported last week that they believed UK house prices would drop by at least 2% (and in some areas 5%) in 2021.

I find it fascinating the Thornton-Cleveleys property market has defied the doom and gloom swamping the wider British economy in the last seven months. The Thornton-Cleveleys property market has profited from the large swell in demand from better-off existing Thornton-Cleveleys households trying to buy larger Thornton-Cleveleys houses (as they are required to work from home) together with the added benefit of saving money from the Stamp Duty Holiday.

Thornton-Cleveleys house prices are 7.3% higher than a year ago, making our local authority area the 60th best performing (of the 396 local authorities) in the UK.

With the Brexit deal being voted through in the Commons on the 30th December, many say this will boost the property market just as the Government-backed measures supporting the property market come to an end. Yet, in the face of rising unemployment due to the pandemic, the Brexit deal may do little more than avoid uncertainty for the Thornton-Cleveleys housing market.

What will happen to Thornton-Cleveleys house prices?

The Thornton-Cleveleys property market in 2019 was held back because of the uncertainty of the Brexit deal. In January 2020, we saw the demand released in the fabled ‘Boris Bounce’, only for buyer and seller activity to fall off a cliff in March during the first lockdown. It then took off like a rocket once lockdown was lifted. UK house prices are 4.19% higher today, year on year (although some areas are breaking the mould, like Aberdeen whose house prices have dropped by 5.1% and at the other end of the scale, Worcester’s house prices have increased by 11.9% year on year). A lot of that growth in UK property prices has been fuelled by buyers spending their stamp duty savings on the purchase price of their new home. Yet, it cannot be ignored.

Of the 44,600 workers in Wyre, 3,300 are still on furlough (although roughly 40% of those people are still only on part-time furlough).

When the furlough scheme ends in April 2021, unemployment is likely to rise to in excess of 11%, whilst the protection for the homeowners utilising mortgage holidays will finish.

Piloting the rocky shoreline of the recession is more important than any Brexit deal for Thornton-Cleveleys homeowners, buy-to-let landlords, buyers and sellers.

In April, the market will also be dealing with the end of the Stamp Duty Holiday, which is due to come to an abrupt halt on the 1st April 2021. Consequently, we will continue to see the house price index’s show growth in the first half of 2021. They will then recede as the prices of Thornton-Cleveleys homes purchased after the 1stApril 2021 reflect the lower price paid (because buyers would have had to pay for their stamp duty again). Therefore, probably by the end of 2021, the Halifax may be correct, and Thornton-Cleveleys house prices will be 2% to 5% lower than they are today, simply because of the stamp duty.

What will happen to mortgage rates?

The real benefit from the Brexit deal is that there will be no tariffs on most goods coming into the UK. 52% of all goods imported into the UK are from the EU (totalling £374bn per annum). The UK Government were planning to add between 2% and 10% tariffs under World Trade Organisation rules on the vast majority of those goods. Price increases because of those tariffs would have fuelled inflation, meaning the Bank of England would have to increase interest rates. Although 77.2% of British mortgages are on fixed rates (paying an average of 2.16%), eventually those increased Bank of England rates would have fed through into higher mortgage payments. To show you how vital low interest rates are …the average Thornton-Cleveleys homeowners’ mortgage is£252.09 pm, owing an average of £102,777.

Yet if interest rates rose only 1.5%, Thornton-Cleveleys homeowners’ monthly mortgage payments would rise to £380.56 pm, and if interest rates were at their 50-year average, then the mortgages payments would be an eye-watering £741.14 pm (note all mortgage payment figures mentioned above are only for the interest element of the mortgage- the capital repayment element would be additional and variable depending on the length of mortgage).

As I have mentioned many times in the articles I have written about the Thornton-Cleveleys property market, low interest rates are vital to ensure we don’t have a property market crash. That’s not to say just because they are at an all-time low of 0.1% to aid the economy that there won’t be some form of realignment of property prices later in the year (as mentioned above). Yet low interest rates mean people can still pay their mortgages, so there won’t be panic selling. That would mean there won’t be a flood of property come to the market (like there was in the 1988 and 2008 property crashes when interest rates were much higher), suggesting property prices should remain a lot more stable.

…and securing higher rents and securing ‘better’ Tenants for your Investment

We at Martin and Co Blackpool, St Annes and Lancaster LET properties quicker then any other agent across our offices. In this post we share some techniques for you to Let your property quicker, secure higher rent and make your property appeal to a wider range of tenants.

Works and modernise

Yes, finances is a hurdle. As a Landlord you don’t want to spend too much doing up your property, which exceed the potential long term returns and as a Landlord due to the high demand, with doing very little work you will most likely secure a Tenant (chances are not to a great tenant). Hence, there is a fine line we need to work with. Either when you are getting are Property to Let for the first time or getting it ready form a tenant Vacating I would suggest you have a clear list of improvements and always look to try and add value every time. Personally I always re-decorate, tidy up external areas and arrange a professional clean regardless. If you can try and make your property stand out, I always check other properties in the area on the market now and look at how I can make my property stand out and this will mean my Property will be at the forefront when prospective tenants are looking.

21a Victoria Road East, Thornton Cleveleys – Hamza Buy to Let Property

Marketing

Are you over looking marketing? Are you thinking how you can make your property look more attractive? As mentioned earlier, it is vital the property is in a suitable condition and then the next stage you present the property in its best light. Professional photography is standard at our Agency and I would highly recommend this. We have done more lets then previous years and during the last year we have been battling with lockdown restrictions, we put this down to a significant push from our side ins regards to videos and virtual tours. Both options are quite simple to do, please see example of both below:

Now we have a great looking property and great marketing, now its time to get your property out there. A good Agent, will be getting the property out to their applicants, marketing on Propety Portals, social media etc. Below are the main portals we would suggest:

Property Portals – Rightmove, Zoopla and OnTheMarket

Facebook – you can do a post on your wall, share in local property groups and there is also the Facebook Market place where you can advertise houses for sale or for rent

Your network

Closing the Deal

I would suggest you have a couple of viewing slots in mind prior to listing property, so you know when the Property goes live and the interest starts to come in you have a few slots you can offer prospective tenants to Let them know when you have availability to show them around. You will be surprised how easy it is to Let your property with out a physical viewing, if you have a good virtual tour or video walk through.

Now the enquiries are coming through, ensure you are responsive in dealing with the enquiries. Follow up all parties after viewings and ensure you are some commitment from interested parties. Please ensure you are compliant with Tenant Fee Ban Act, which restricts the amount you can take as a holding deposit (one weeks rent) and the restrictions to marketing and considering other applications when a party has expressed interest. Pre-qualify your interested party before any viewing, key points to establish is if this tenant is suitable for this property you have available, if they can afford the rent and if there provisional target move in date fits with what you are looking for.

Follow these steps and you will Let your properties quicker, secure higher rents and hopefully manage to get the best tenant for your property. Martin and Co secure 30% of our Lets within 24 hours, we attribute this success towards through this process we follow.

Roll the clock back to April 2020, and major financial economists and property market commenters were sounding the alarm. The very best-case scenario was a 5% drop in property values by the end of the year, and most were in the 10% to 15% range. They forewarned the Covid-19 stimulated recession would trim tens of thousands of pounds off the value of Blackpool homes.

Yet the Blackpool property market seemed not to get the memo on that, and now as we find ourselves at the end of 2020 and the worst of lockdown restrictions appear to be passed, vaccinations on the way and economy starting to grow, Blackpool property prices seem to be doing quite well.

What happened to the Blackpool house price crash that wasn’t?

Before I answer that, it reminded me of what the Treasury said in 2016 about a leave vote on the Brexit referendum. The considered opinion of the Treasury was house prices would drop by 18% if the country voted to leave the EU, so let us see what that would have done to Blackpool house prices if that had taken place and then what exactly has happened in the last four and half years …

Average Value 2016

Predicted Drop by The Treasury because of Brexit

Average Value Today

Uplift in Value in last 4.5 years

% Increase since Brexit Vote

Blackpool Detached

£210,600

£172,700

£243,700

£33,100

16.7%

Blackpool Semi-detached

£128,100

£105,000

£142,700

£14,600

10.4%

Blackpool Terraced / Town House

£98,100

£80,400

£104,200

£6,100

7.2%

Blackpool Apartments

£80,800

£66,300

£93,100

£12,300

14.3%

So why has the Blackpool property market not matched the property pundits twice in the last five or so years?

Well for most of us, owning a property is about having somewhere to live rather than an investment (an Englishman’s home is his castle??). Nevertheless, once a homeowner is on the proverbial ‘property ladder’, it cannot be denied that it is eternally beneficial to know, as a homeowner, that you have made a healthy investment in your home and that the value will rise to alleviate the ache of trading up market – or down market when you retire.

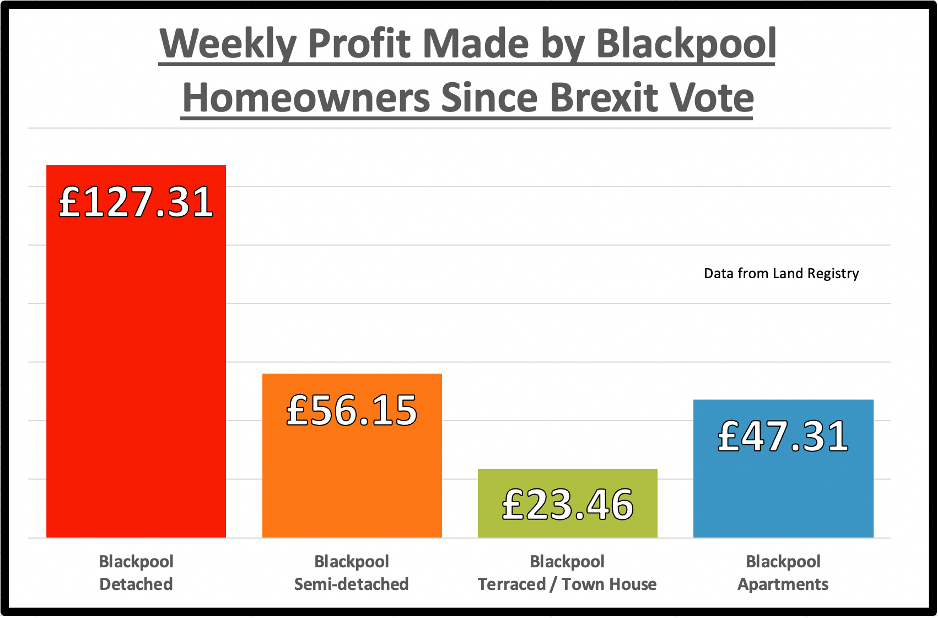

Those Blackpool homeowners who own detached homes would have made an average of £33,100 profit, a rise of 16.7% or a weekly profit of £127.31 – calculated between the price they would have paid in the summer of 2016 and the price they would sell for today. Looking at the weekly profit for all property types in Blackpool since the Brexit vote…

Blackpool detached homes weekly profit of £127.31 per week

Blackpool semi-detached homes weekly profit of £56.15 per week

Blackpool terraced homes/town homes weekly profit of £23.46 per week

Blackpool apartments weekly profit of £47.31 per week

Whilst it is no surprise the property market boom was inspired by the Chancellor’s Stamp Duty holiday, this is not exclusively the Chancellor’s achievement. The three ‘D’s have been with us throughout 2020, Covid or no Covid (Debt, Divorce and Death), together with a huge shift in the way Blackpool homeowners see their homes. With us cooped up during the lockdown and working from our dining room tables, the want and need of Blackpool people to have a home with an extra bedroom to work from, together with a garden, has been one of the most challenging this year… hence the rise in demand.

So, what of 2021? It’s true that the country will have high unemployment, yet at the same time, we have ultra-low interest rates and for the last 20 years, on average we have only built 150,000 households per year as a nation, but needed 300,000 per year to keep up with immigration, people living longer and changes in the way households are made up (compared to the Millennium).

Many people can predict what will happen – yet none of us really know what will actually happen to the Blackpool property market in 2021.

Covid was a black swan event and the fallout from that, I believe, has changed Blackpool peoples’ lives and their lifestyles, especially how they see their home. Instead of making predictions, nothing can get away from property market fundamentals, which have driven price booms on the back of high demand for homes and low supply (i.e. properties coming onto the market) and price crashes on the back of over-supply and low demand. Only time will tell if, in 2021, the Blackpool property market will see a flood of properties coming to the market because of debt or the demand for larger homes continues to rise unabated.

12 months ago, the unemployment rate in Blackpool stood at 6.6% of the working population, yet with Coronavirus hitting the UK, what impact will this rise in unemployment have on the Blackpool property market?

As I have discussed a number of times in my articles on the Blackpool property market, this summer saw the Blackpool property market do exactly the opposite of what was expected when Covid hit.

The Stamp Duty holiday added fuel to pent up demand for people to move to property with extra rooms (to work from home) and gardens. This prompted a brief hiatus in the number of people selling and buying their home in Blackpool over the last summer and autumn.

Yet, insecurity around rising unemployment, led to many mortgage companies becoming more cautious in the later months of summer, predominantly when lending to self-employed or first-time buyers borrowing more than 85% of the value of the home (as they wouldn’t want to lend money to someone that could not afford a mortgage due to an insecure income or not having a job).

Back in the late spring, economists were predicting that UK unemployment would rise to a peak of 6.5% in Q3 2020, returning back to the 2019 levels (3.4%) by 2022.

As we speak (Christmas 2020), nationally the unemployment rate stands at 6.3%. The toll Covid has had on people’s livelihoods has been massive, with an additional 1,434,515 people out of work, although it is important to note this unemployment rate is still lower than the five years following the Credit Crunch years 2008 to 2013.

So, with such a growth in unemployment and the spectre of a ‘No Deal Brexit’, this may hold back the enthusiasm of many companies to take on more staff, reducing any rebound in employment. If unemployment remains high, this will influence perceptions of employment and personal/household financial security, which are the ultimate drivers both for house prices and whether people buy and sell.

5,520 Blackpool people were unemployed a year ago and today that stands at 9,875.

Looking at all the study papers on the topic, there is a link between unemployment and house prices, yet it’s not as strong as you would think. The larger factors are the demand and supply of property on the market and interest rates. Interestingly, in the past two recessions, the comparatively richer regions of London and South East, house prices have been more sensitive to unemployment and house price changes than the rest of the UK, yet London and the South East also bounced back quicker and higher after the two recessions.

The concept behind this is that more expensive house prices in the South drop more than lower priced houses in the rest of the UK. Why? Because those more expensive regions have, by definition, more expensive house prices meaning the homeowners have higher mortgages, so if they become unemployed, their homes are more likely to be repossessed (because of the high mortgages), and consequently that reduces house prices in that area quicker because repossessed houses tend to sell much more cheaply compared to normal house sales.

The health of the Blackpool property market in 2021 and beyond really depends on what is happening to the economy as a whole and more specifically what is happening in the Blackpool economy.

When we drill down though, unemployment has hit different sectors of the economy to a lesser or greater extent. For example, for office workers, people who work in tech, sciences and the professional services, the impact on jobs has been comparatively mild, with many personnel able to work from home. Yet for others, such as those who work in the hospitality, leisure, retail, entertainment and catering industry, remote working is simply not an option and these have been hit the hardest.

Unfortunately, the industries mentioned above are the ones that tend to employ the younger generation, who invariably live in private rented accommodation, rather than own their own home. Being made redundant puts their dream of buying their first home back even further as they try and get themselves back on their feet by initially finding a job (let alone save for a deposit).

Housing markets will recover quickest in towns and cities, where jobs are in the more resilient employment sectors.

For example, in London, unemployment jumped really quickly (and high) in 2009 with the Credit Crunch, yet came down just as quick in 2011, just as the property market in London started to take off, whilst in Blackpool, it took a lot longer for unemployment to drop and the Blackpool property market didn’t really start to get going until 2013/14.

If we have a determined economic contraction, with a lengthier and leisurely economic recovery, impeded by financial stress, that will lead to much higher unemployment in the 10% to 12% range in the summer of 2021. However, before I get to the initial question, I need to highlight another interesting fact, because…

What is particularly interesting is the increase in unemployment in Blackpool amongst men has been higher than women, with a growth of 6.7 percentage points for men compared to 3.5 percentage points with women.

So, what is the prediction for the Blackpool property market under the cloud of this growth in unemployment?

One massive redeeming factor that could just save the Blackpool property market is low interest rates. This will keep mortgage payments low, meaning repossessions should be kept to a minimum (therefore there shouldn’t be a flood of cheaply priced Blackpool properties coming onto the market all at the same time and dragging Blackpool house prices down with it, as it did in the previous two recessions of 2009 and 1989).

Yet, irrespective of the ultra-low interest rates, I still consider property prices in Blackpool at Christmas 2021 won’t be much different from today, and in fact could be slightly lower.

This is because people have been paying top dollar in the last six months to secure their dream Blackpool home, quite often spending the money they saved on Stamp Duty on the purchase price. When Stamp Duty Tax returns in April 2021, there will be less money to pay for the property … thus Blackpool property values will be, by implication, lower in a year’s time.

What about Blackpool landlords and the rents?

Nationally, rents fell just over 2.3% between 2008 and 2010, following the Credit Crunch, while national house prices fell 15.9%. I anticipate Blackpool rents will also remain comparatively robust in the coming months and years.

Rents are very much tied to the rise and fall of wage growth and I can’t see why this relationship shouldn’t continue. Rents will rise in Blackpool by between 13% and 15% in the next five years, yet if property prices do rise in 2023/24, that means future rental yields will be marginally lower in 2023/4 comparative to today, especially as ultra-low interest rate expectations (according to the money markets) seem to be here to stay for a long time.

Therefore, something tells me there could be some interesting Blackpool buy-to-let investment opportunities for Blackpool investors willing to play the Blackpool buy-to-Let market for the long term.

To conclude, these are just my personal opinions. If you are a Blackpool landlord looking for advice and opinion on what to buy to maximise your returns, please don’t hesitate to contact me. If you are a Blackpool homeowner, looking to buy or sell and need any advice or an opinion on where the market is and where your Blackpool home sits in the bigger Blackpool property market picture – again feel free to drop me a line.

Voids (time in between tenant vacating and new tenant moving in) are a massive bugbear for me and I feel it is one of the most overlooked expenses you as a Landlord would incur. I did a post on Voids as a whole and ways to reduce costly void periods earlier this year, article can be found on the link below: https://blackpoolpropertyblog.com/2020/05/16/7-days-of-landlord-tips-1-voids/

In this article I wanted to cover of Council Tax exemptions during void periods. One area I see Landlords fail is notifying the council of your new tenant moving in and vacating, with exact dates and names. I would always recommend to do this via email so there is a record. if this doesnt get done it can lead to issues with future payments of council tax and incorrect invoicing being issued from the Local Authority due to no or incorrect information from the on-set. If you are using a Managing Agency they would do this for you in between tenancies, along with notifying the utility providers.

I have summarised the discount from each council, please note this is if the property is unfurnished (white goods are allowed). The council tax exemption period can be applied in between each change in occupation, subject to the occupation being for a minimum of 6 months. Most people have a perception that a council tax exemption can only be claimed once during the financial year, which isn’t the case.

Councils have now also introduced an additional premium charge if the property has been empty for more than 2 years, with most councils electing to charge 100% extra in council tax.

If you are going to be doing major work at the property, it is worthwhile to consider you can claim for an exemption if the property is classed as ‘inhabitable’ and undergoing major works. This again varies from council to council, for example in Blackpool this isn’t possible to be claimed, but for a property under Wyre council you can claim upto 12 month exemption. As part of this process you will be required to submit evidence showing the works and demonstrating the property is inhabitable.

For the Serviced Accomodation providers out there, you can potentially pay 0 council tax! What Landlords in the serviced accommodation model sometimes forget to realise is that you are operating a business and small businesses benefit from small business rates relief (up-to a rateable value of £16 000). Most Serviced Accomodation units will fall under the the £16 000 rateable value, hence meaning you can benefit from an exemption in this scenario. To benefit from this exemption you need to change the council tax banding so the property is rated under commercial business rates as opposed to domestic rates.

To summarise, be conscious of potential council tax bills you will incur when property is empty. Ensure you have claimed your necessary exemption. Notify council of any changes of tenancy.